Editor's Note: Take a look at our featured best practice, Pricing Strategy (38-slide PowerPoint presentation). Pricing Strategy is a core pillar of Marketing and Product Strategy. It is 1 of the 4 Ps of Marketing (also known as the Marketing Mix - Product, Price, Placement, and Promotion). As such, knowing how to properly price your product is extremely important to the commercial success and viability of [read more]

* * * *

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of Target Costing. Target Costing is referred to as an organized process to determine the cost at which a proposed product must be developed so as to generate profits at the product’s anticipated selling price in future.

In highly competitive markets such as FMCG, construction, healthcare, and energy, prices are determined by market forces. Producers cannot effectively control selling prices. The only control, to some extent, is over costs, so management’s focus has to be on influencing every component of product, service, or operational costs.

Target Costing is a proactive Cost Planning, Cost Management, and Cost Reduction practice. Costs are planned and managed out of a product and business early in product life-cycle, rather than during the later stages. The fundamental objective of Target Costing is to make the business profitable in any competitive marketplace. Target Costing is widely used in several industries e.g. manufacturing, energy, healthcare, construction, and a host of others.

Some key features of Target Costing are:

Seller is a price taker rather than a price maker.

The target selling price incorporates desired profit margin.

Product design, specifications, and customer expectations are built-in while formulating the total selling price.

Cost reduction and effective cost management is the corner stone of management strategy.

Target Cost has to be achieved through team collaboration during activities such as designing, purchasing, manufacturing, marketing, and other activities.

Target Costing presents the following advantages over other product pricing techniques:

More value delivered to customer since the product is created keeping in mind the expectation of the customer.

Approach to designing and manufacturing products is market driven.

New market opportunities converted into real savings to achieve the best value for money rather than to simply realize the lowest cost.

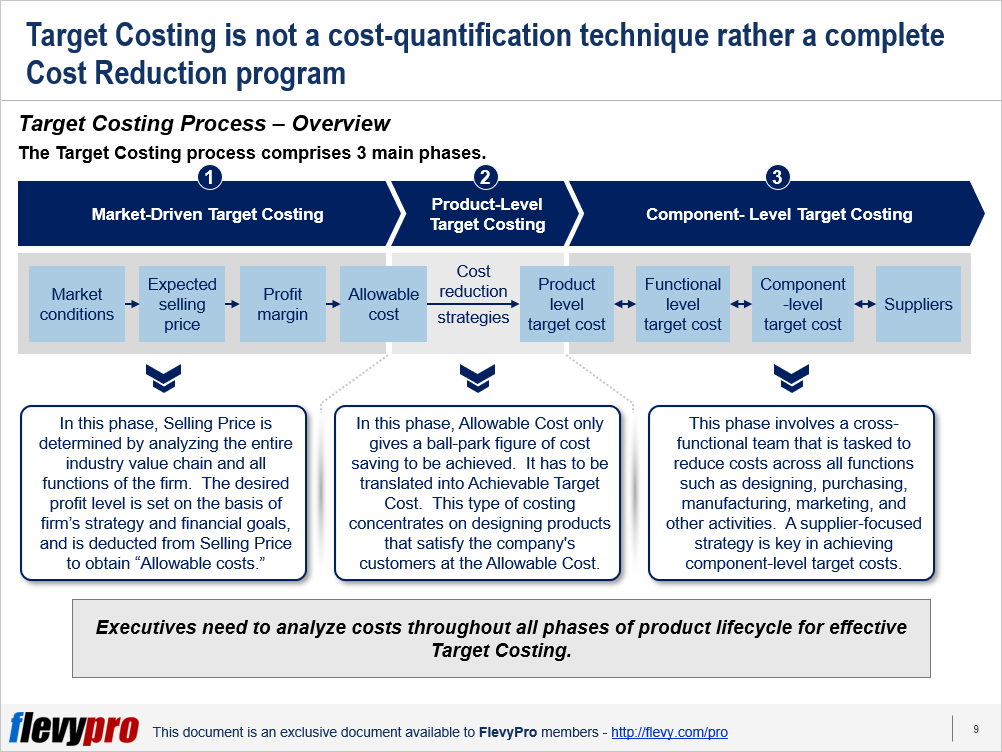

The Target Costing process comprises 3 main phases.

Market-Driven Target Costing

Product-Level Target Costing

Component-Level Target Costing

Let’s discuss the 3 phases briefly.

1. Market-Driven Target Costing

In this phase, Selling Price is determined by analyzing the entire industry value chain and all functions of the firm. The focus of this costing phase is on analyzing market conditions and determining the company’s Profit Margin in order to identify the “Allowable Cost” of a product.

In this phase, the desired profit level is set on the basis of firm’s strategy and financial goals, and is deducted from Selling Price to obtain Allowable costs. Intensity of competition, nature of customers, similar product introduction by competitors, and level of customer sophistication are the key factors influencing Market-driven Target Costing.

2. Product-Level Target Costing

In this phase, Allowable Cost only gives a ball-park figure of cost saving to be achieved. It has to be translated into Achievable Target Cost. This type of costing concentrates on designing products that satisfy the company’s customers at the Allowable Cost. The cardinal rule of Product-level Target Costing is to never exceed the Target Cost.

The objective of this Target Costing phase is to create intense but realistic pressure on the product designers to reduce costs. Product Strategy (number of products in the line, frequency of redesign, degree of innovation) and product characteristics (complexity, magnitude of up-front investments, and duration of product development) are the key factors affecting Product-level Target Costing.

3. Component- Level Target Costing

The Component-level Target Costing settles the price at which a firm is willing to purchase the externally-acquired components being used in its product. This phase involves a cross-functional team that is tasked to reduce costs across all functions such as designing, purchasing, manufacturing, marketing, and other activities.

The components cost history serves as the starting point for estimating the new component-level target costs alongside optimal selection of suppliers. A supplier-focused strategy is the key factor that influences Component-level Target Costing.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“As a small business owner, the resource material available from FlevyPro has proven to be invaluable. The ability to search for material on demand based our project events and client requirements was great for me and proved very beneficial to my clients. Importantly, being able to easily edit and tailor the material for specific purposes helped us to make presentations, knowledge sharing, and toolkit development, which formed part of the overall program collateral. While FlevyPro contains resource material that any consultancy, project or delivery firm must have, it is an essential part of a small firm or independent consultant’s toolbox.”

– Michael Duff, Managing Director at Change Strategy (UK)

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

“Several times a month, I browse FlevyPro for presentations relevant to the job challenge I have (I am a consultant). When the subject requires it, I explore further and buy from the Flevy Marketplace. On all occasions, I read them, analyze them. I take the most relevant and applicable ideas for my work; and, of course, all this translates to my and my clients’ benefits.”

There are 3 common approaches to pricing: Cost-based Pricing, Competitive Pricing, and Value-based Pricing.

Value-based Pricing offers numerous distinct advantages over the other 2 pricing methodologies. It is particularly suitable for situations where you are entering a new market, offering a [read more]

Readers of This Article Are Interested in These Resources

As core markets become saturated with new entrants and products, we find it more and more difficult to grow the core. We find traditional approaches that have successfully driven growth historically are also reaching points of diminishing returns.

Business Model Innovation (BMI) is a powerful, [read more]

Pricing products and services is one of the most complex and overlooked elements of a strategy. This document provides a guide and framework to help build better understanding of different strategies and tactics available.

Areas covered include:

Why is pricing important?

Pricing Strategy [read more]

This is a presentation used for conducting a pricing workshop for your organization or a client's. It covers, among others, the following:

- Pricing framework & Implementation

- OEM pricing

- Distributor pricing

- New product pricing

- Bundle pricing

The presentation has 130 slides.

See [read more]

This toolkit is focused on the point at which we actually ask the customer for a price increase. None of the strategic value of a pricing recommendation matters unless we take action with the customer. There are several tools and approaches that could make the increase more successful.

This [read more]

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of