Editor's Note: Take a look at our featured best practice, Comprehensive Guide to Financial Statement Analysis (89-slide PowerPoint presentation). This document provides a detailed step-by-step guide on how to analyse financial statements. Designed for anyone who wants to understand how to review financial data and interpret the findings, the document is split into the following sections:

Introduction to financial statements

1. Income [read more]

* * * *

Financial statement analysis can be referred as a process of understanding the risk and profitability of a company by analyzing reported financial info, especially annual and quarterly reports. In other words, financial statement analysis is a study about accounting ratios among various items included in the balance sheet.

Advantages of Financial Statement Analysis

The different advantages of financial statement analysis are listed below:

The most important benefit if financial statement analysis is that it provides an idea to the investors about deciding on investing their funds in a particular company.

Another advantage of financial statement analysis is that regulatory authorities can ensure the company following the required accounting standards.

Financial statement analysis is helpful to the government agencies in analyzing the taxation owed to the firm.

Above all, the company is able to analyze its own performance over a specific time period.

From the above, it is obvious that only way for financial analysis is ratio analysis.

What is Ratio analysis?

What is the role/Importance of ratio analysis in financial analysis?

What are its advantages?

How it helps out in decision making?

How it helps the auditor in assessment of the risk of material misstatement?

These are some questions the answer of each must be known by every professional, business man and by user of financial statement. Some of you may already know about these. The answer of these questions must be part of professional’s life and business man must know to keep check on the management progress.

In simple words, we can say that ratio analysis is “quantitative analysis of information contained in a company’s financial statements.” In fact, it is critical quantitative analysis.

Ratio analysis helps to understand about business:

Its performance and financial position,

Its strengths and weaknesses,

Its opportunities,

Its threats, and

To make reasonable forecasts about its performance in coming period.

Horizontal analysis (it is analysis on the basis of previous year) helps to identify its performance. On the other hand, vertical analysis helps to identify its strength, weaknesses, and others facts.

Among other functions, one of the most important functions of ratio analysis is to act as indicators in identifying positive and negative financial trends (fluctuation in its performance). Trend analysis helps to implement ongoing financial plans and guiding to give input more rigorously at selected areas. Like either to increase sale or reduce cost etc. It also helps to make corrections to short-term financial plans. Like if have surplus cash either to invest in commodities or in financial instruments. Comparability of financial information is one of the ideal approaches to judge business performance. You can either compare the financial state of your business against other businesses within same industry or to compare financial results with previous year. However it is worth to remember that comparing numbers side-by-side does not always provide businesses with a way of determining if their financial position has become better or worse. Instead, ratio analysis in accounting allows businesses to place data in manageable terms in order to better understand their position. This also causes businesses to break their financial data into parts so that they can recognize any weaknesses, opportunities or threats. While most ratio analysis in accounting is used to determine the business’s current position, some ratios can be used to make financial predictions. The numbers of available financial ratios makes it important to research and choose option most applicable to your business under the current scenario.

Ratio analysis use historical data in order to understand the business’s past and current financial position. Data for ratio analysis contained in your own previous year financial statements and/or financial statement of other businesses in the same industry, which might be competitor of your business.

By ratio analysis, it may come to notice that business is purchasing more inventory than is needed, which is preventing it from using cash to finance in the development of other products. It might also come to notice that business is missing investing opportunities by holding much cash than its need. Wise business units and industries which make periodical review of their financial strength, commonly asked by decision makers to tract trends and notice weaknesses or opportunities immediately.

Remember when conditions do not fluctuate reasonable predictions can be made about the future. For instance, businesses create a common sized income statement to show all of the amounts on the income statement as a percentage of sales after it compare these statements historically for trend analysis. Once a trend has been built, it can predict what will happen or what can be achieved. Suppose if the selling expenses are increasing consistently by 3.2% each year, a business can reasonably assume that it will increase by the same ratio and sale will also increase by the same trend.

Purpose of Ratio Analysis

Ratios are worked out to analyze the following aspects of a business enterprise:

Solvency (Long term and short term)

Profitability (With the help of profitability ratios)

Operational efficiency (As turnover ratios)

Credit standing

Effective utilization of resources

Investment analysis

Remember two main objectives or goals of every business are, as below:

Solvency; and

Profitability.

If business fails to manage any of two, then consequences could bring your business to shut down. As effective these two business assertions are managed the question of “either your business is going concern or not” going farther from your mind.

Solvency Ratios

Balance sheet is the key to check the solvency of a business unit. These financial ratios focus on calculating each asset on the balance sheet as a percentage of total assets and each liability as a percentage of total liabilities plus owner’s equity. Calculating and comparing for corresponding reporting periods in two consecutive years helps to identify trends such as decreasing cash and increasing accounts receivable balances, debtor collection period is reducing. Financial planning goals might then include strengthening your accounts receivable collection policy and tightening credit-granting guidelines.

Profitability Ratios

Profitability ratios are expressed in %age and show financial performance of your business in %age not the financial position. Like G.P ratio, CGS ratio, Operating expense ratio, Net profit ratio etc. A professional, business man and users of financial statement will judge the causes of losses in variant ways. A professional want to know and to state in report the causes of loss or causes of profit at lower %age. Business man has concern how cost can be controlled while the users of the financial statement will take trend analysis to make decision about investment in company.

Turnover and Efficiency

Operating expense and turnover ratios are most critical for helping you to assess how efficiently your business is utilizing assets and managing its liabilities. Turnover ratios typically need deeper analysis, with both extraordinarily high and low ratios indicating a cause for concern. For example, a high inventory turnover ratio indicates a need to review the inventory budget, because your business could be losing sales due to frequent stock-outs if stocks not properly managed. Your stock level is linked to your production schedule. Similarly asset turnover tells you how much efficient your assets.

Cash and Liquidity

Cash and liquidity ratios help determine whether you can afford to invest or you can afford for long-term business growth. A current asset ratio, Liquid asset ratio and working capital all are useful for assessing whether your business has enough liquidity to pay for daily operating and short-term debt expenses, like interest. For instance, a current ratio compares current assets to current liabilities. A ratio of 2 to1 shows your business is sufficiently liquid. At this stage, you can initiate for investment in capital market or to take steps for investments into your financial plan.

Auditor’s Concern about Ratio Analysis

Remember auditor has limited concern or usage of ratios for audit purposes only, to issue report. Auditor is only supposed to check the accuracy and presentation of financial transactions in correct manner. Auditor uses (ratios) as analytical procedures at three stages during audit of the financial statements (financial statements are the responsibility of management not of auditor).

As risk assessment Procedures

Analytical procedures are performed at initial stage of the audit to help the auditor to obtain an understanding of the entity and to assess the risk of material misstatement. Then audit procedures can be directed to most risky areas.

As Substantive Procedures

Auditor use analytical procedures as substantive procedures in determining the risk of material misstatement at assertion level during work on income statement and balance sheet.

At the end of the Audit

Analytical procedures performed at the end of the audit in forming the overall conclusion as to whether the financial statements are in accordance with the auditor’s initial understanding or not.

Now, we will take a hypothetical example and will take analysis as an auditor, as business owner and user of the financial statements.

Auditor’s Concerns about Financial Statements via Analytical Procedures

If we see the progress of entity in the year 20X2 overall results has been changed. Company made progress from net loss to profit. It may be caused by any of the following two reasons:

Company has performed efficiently.

Company has fraudulently set the financial statement to deceive the users of the financial statements.

Note that auditor always perform the audit by keeping in mind the professional skepticism and will focus on cause b as stated above.

Sale has been increased only by 17% and that administrative expenses appear low. So there are chances that expenses are intensely less stated.

Cost of sales fall by 17% which shows unusual trend. Because sales has been increased by 17% while cost of sales has not been increased proportionately.

GP% is 53% in the year 20X2 while it was 33% in previous year. To identify the reasons of this change auditor will focus and will extend audit procedures on sale and cost of sale.

Selling and distribution expenses have been increased by 42%. It is not increased in proportion to the sales. There may be misallocation of expenses.

Interest payable has been fallen but at a small ratio. It shows interest has not been paid during the period. While there is surplus cash. This amount may be overstated or may be a new loan has been obtained from financial institution. The auditor shall investigate the reason about failure of non-payment or else.

Investment income is new in this year. It shows there is out flow in cash and cash equivalents. There is possibility of errors or other income generating assets has not been disclosed. There is possibility that interest payment factor was ignored while management kept focus on investment to show progress.

Directors and User of the Financial Statements Analysis

Both will argue in their own point and will be satisfied to see about the increased amount of sale. They will perceive that organization is performing well and generating more revenue than previous year.

Regarding cost of sales they will predict that management has controlled overheads. But an owner or knowledgeable investor will investigate about the causes of reduction in cost of sales. But it is presumed that management has fraudulently prepared and presented the financial statements because there is reduction in cost.

In the same way both will perceive about Gross profit (GP is increased) as they perceive about increase in sale.

Selling and distribution expenses have been increased. It will satisfy the owner to ensure about the management efforts to generate more revenue. More optimistic effort caused to incur more expense.

Interest payable may be against short term loan. Both will not be worried about the payment because business has surplus cash and cash equivalents.

Investment income must be in proportion to the investment shown in balance sheet at bench mark rate. Both will be happy to see the investment income. User of the financial statement will take decision in positive response.

Conclusion

Matter was not to discuss the ratios. Matter was to know about the objectives which are different of each. But all make decisions with the help of ratio analysis. So think analytically you will be able to make better decision in your professional career. There are many businesses (Ltd companies situated in my own city, FSD-PAK) who are suffering from financial crisis due to inappropriate investment or inappropriate financing decisions.

This document explains the financial statement analysis process. Most slides are instructional and covered topics include the financial statement analysis process, financial ratios analysis, accounting information (assumptions, principles, policies, procedures), and others.

Financial [read more]

Do You Want to Implement Business Best Practices?

You can download in-depth presentations on Financial Analysis and 100s of management topics from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives.

For even more best practices available on Flevy, have a look at our top 100 lists:

These best practices are of the same as those leveraged by top-tier management consulting firms, like McKinsey, BCG, Bain, and Accenture. Improve the growth and efficiency of your organization by utilizing these best practice frameworks, templates, and tools. Most were developed by seasoned executives and consultants with over 20+ years of experience.

Readers of This Article Are Interested in These Resources

Evaluating Financial Ratios (or Financial Comparables) is a crucial method for evaluating the financial and competitive health of a company relative to its competitive peers. This document provides an overview to Financial Analysis, as well as deep dive into 20 widely used Financial [read more]

User friendly and easy customizable guide to the world of Financial Ratios and Valuation Multiples.

A must have Financial tool for anyone performing Financial Modeling and Financial Analysis.

The template is a detailed guide of Financial Ratios and their application on Financial Statements and [read more]

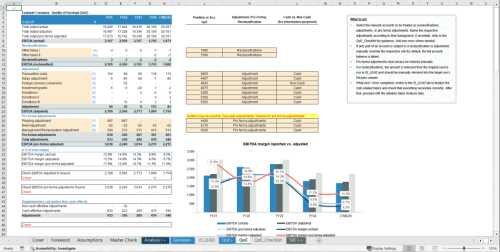

Purpose of the tool

This Excel-based Quality of Earnings (QoE) Model provides a structured framework to analyse the underlying earnings quality of a business by reconciling reported financials to adjusted and pro-forma results. It enables you to capture and classify reclassifications, [read more]

Curated by McKinsey-trained Executives

PART I: THE EVOLVING ROLE OF THE CFO

1. The Strategic Imperative of the Modern CFO

• 1.1 The CFO as a Corporate Strategist

• 1.2 Navigating the C-Suite: Board and CEO Collaboration

• 1.3 CFO vs. Controller vs. Treasurer: Distinctions and [read more]

Horizontal analysis (it is analysis on the basis of previous year) helps to identify its performance. On the other hand, vertical analysis helps to identify its strength, weaknesses, and others facts.

Horizontal analysis (it is analysis on the basis of previous year) helps to identify its performance. On the other hand, vertical analysis helps to identify its strength, weaknesses, and others facts. Ratio analysis use historical data in order to understand the business’s past and current financial position. Data for ratio analysis contained in your own previous year financial statements and/or financial statement of other businesses in the same industry, which might be competitor of your business.

Ratio analysis use historical data in order to understand the business’s past and current financial position. Data for ratio analysis contained in your own previous year financial statements and/or financial statement of other businesses in the same industry, which might be competitor of your business. Remember two main objectives or goals of every business are, as below:

Remember two main objectives or goals of every business are, as below: