Editor's Note: Take a look at our featured best practice, Private Credit Fund - 10 Year Financial Model (Excel workbook). A private credit fund is an investment vehicle that provides loans directly to businesses outside of public bond markets, typically targeting middle-market companies and special situations where flexible, customized financing is valued. The fund earns returns primarily through interest income, [read more]

* * * *

You’ve built a business from scratch and a home to match: now it’s time to let one power the other.

You’ve built a business from scratch and a home to match: now it’s time to let one power the other.

Your next product launch or equipment upgrade isn’t waiting on a loan officer’s approval. It’s already within reach, sitting in your home equity. While banks still cling to W-2 logic, self-employed pros are rewriting the rules; tapping into the value they’ve built to fund the growth they’re chasing.

You don’t need permission to scale. You need a smarter way to unlock capital. Let’s get into how your home can help bankroll your next business move.

Why Traditional Business Loans Miss the Mark for Solopreneurs

Banks and credit unions typically underwrite business loans based on employer history, W-2 income, and a predictable cash flow, all of which self-employed professionals may lack in traditional forms. Even when a freelancer or business consultant brings in six figures, fluctuating month-to-month income and unconventional tax filings can paint an incomplete financial picture to underwriters. As a result:

- Application rejection rates for self-employed professionals are disproportionately high

- Lenders may impose higher interest rates to hedge perceived risk

- Funding timelines can stretch out just when agility matters most

- Borrowers may be asked to provide extensive documentation that isn’t applicable to their business model

The equity built into a primary residence represents a tangible, low-cost asset that can serve as a lifeline for business expansion, equipment upgrades, marketing campaigns, or simply creating a longer runway between client payments.

How HELOCs Work for Self-Employed Borrowers

A home equity line of credit gives you credit guaranteed against the equity in your home. Unlike a lump-sum loan, a HELOC operates more like a credit card with a borrowing limit, only with significantly lower interest rates. The borrower draws funds when needed and repays only what they use, often with interest-only payments during the draw period.

For self-employed professionals, this flexibility can make all the difference when:

- Navigating seasonal income cycles

- Investing in tools, software, or workspace upgrades

- Hiring contractors or part-time help during growth spikes

- Covering upfront costs for projects that won’t pay out for weeks or months

Working with a home equity line of credit lender that understands non-traditional income and provides tailored underwriting for self-employed borrowers is essential.

Smart Use Cases: When Leveraging Home Equity Makes Strategic Sense

Not every expense justifies tapping into home equity, but it can serve as a low-friction way to leap ahead. High-value use cases might include:

- Launching a new product line with a limited run and market testing

- Funding content production or digital advertising to grow customer acquisition

- Securing certifications or advanced training to expand services

- Remodeling a home workspace to support productivity or compliance

- Acquiring a business vehicle or specialized equipment

Because HELOCs typically come with variable interest rates, they’re best suited for short-to-medium-term investments that will generate a return within a few years.

Evaluating Risk and Timing

Equity-backed financing is not a decision to make lightly. Business owners must weigh the upside of immediate capital access against the obligation of a secured debt as part of their business plan. Important considerations include:

- Current loan-to-value ratio and how much equity is realistically available

- The ability to absorb variable payments if rates rise

- Whether your business has a track record of ROI on past investments

- Exit plans for the debt, especially if business cash flow slows

Alternatives to Explore if Equity Isn’t the Best Fit

While HELOCs offer attractive terms, they aren’t a one-size solution. Other financing paths may include:

- Business credit cards with promotional APRs and points-based rewards

- Equipment leasing with deferred payment options

- Invoice factoring to convert receivables into instant cash

- Crowdfunding for marketable product ideas

- Peer-to-peer lending platforms that assess business viability beyond credit score

Your House Can Fund Your Hustle

A well-managed HELOC is more than a lifeline. It’s a flexible growth tool for self-employed professionals who’ve built equity not just in their homes, but in their ideas. It opens the door to funding on your terms without handing over a chunk of your company, overpaying in interest, or navigating endless underwriting checklists. When used with intention and a clear plan for ROI, tapping into home equity can be the smartest move a self-starter makes.

49-slide PowerPoint presentation

Hybrid Financing: Preferred Stock, Warrants, and Convertibles

Lecture Outline

1. Types of hybrid securities : Preferred stock. Warrants. Convertibles

2. How does preferred stock differ from common stock and debt?

3. What are the advantages and disadvantages of preferred stock

4. What is

[read more]

Do You Want to Implement Business Best Practices?

You can download in-depth presentations on Financing and 100s of management topics from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives.

For even more best practices available on Flevy, have a look at our top 100 lists:

These best practices are of the same as those leveraged by top-tier management consulting firms, like McKinsey, BCG, Bain, and Accenture. Improve the growth and efficiency of your organization by utilizing these best practice frameworks, templates, and tools. Most were developed by seasoned executives and consultants with over 20+ years of experience.

Readers of This Article Are Interested in These Resources

Excel workbook

MODEL OVERVIEW

An Equity Private Placement (EPP) involves the sale of equity to one or more investors with the purpose of raising capital for business expansion, working capital or strategic initiatives and/or enabling existing shareholders to realize returns on their equity. An equity

[read more]

Excel workbook

Most startups are initially financed by their founders. They contribute relatively small amounts of money for the company to make its first steps. If the business idea proves feasible, there will be the first real funding round ("seed" funding) when the company receives financing from external

[read more]

56-slide PowerPoint presentation

Private equity ("PE") pool funds of capital invested in businesses, which come with a fixed investment horizon, at which point the PE firm exits the investment. Exit strategies include IPOs and the sale of the business to another PE firm or strategic buyer.

PE funds are focused on the

[read more]

Excel workbook

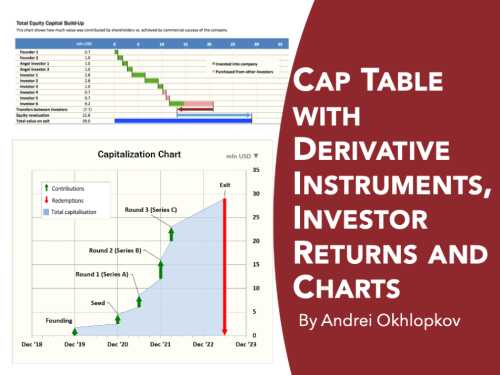

User-friendly Cap Table Model for a startup company or early-stage venture including multiple rounds of investments and investors returns analysis.

The template is a flexible tool assisting investors in identifying how much venture capital a start-up requires and when based on Discounted Free

[read more]