Editor's Note: Take a look at our featured best practice, Cost Reduction Opportunities (across Value Chain) (24-slide PowerPoint presentation). Though there are multiple levers to maximizing an organization's profitability, costs are the most directly controllable by any organization. Profitability is being challenged by increased costs, stagnated revenue growth, and increased capital costs in today's economic climate.

Therefore, a [read more]

* * * *

Luxury goods lives in an odd tension. Scarcity, story, and soul drive desire, yet the sector runs on complex global operations that must deliver with watchmaker precision. Global luxury spending hovered near 1.5 trillion euro in 2024 and stayed essentially flat as shoppers traded up to experiences, downshifted on entry items, and became picky about value. Bain and Altagamma flag a tougher year, with only about one third of brands growing in 2024 and personal luxury goods roughly flat to slightly down year over year.

That is not doom. That is a reminder that execution beats headlines in this category.

A robust value chain matters because imagination without delivery is just theater. Margin is created or eroded at every hand off, from atelier bench to flagship to clienteling on a messaging app. McKinsey expects fashion and luxury players to generate the largest share of economic profit in the sector, yet notes the environment will test discipline on pricing, cost to serve, and capital allocation. You win when each activity stacks in sync and nothing leaks.

Unveiling the Luxury Goods Value Chain

A value chain is the connected system of activities that turn ideas into products into lasting client relationships. The game in luxury is to protect scarcity and elevate perceived value while moving through that system with near zero friction. Think of it as choreography more than a pipeline.

Craft is the credibility check. Clients forgive delivery lead times if the product feels unmistakably made, not produced. Treat workshops as strategic assets. Map the skill graph, not just capacity, so you can route limited savoir faire to the highest narrative items. Small quality escapes destroy more brand equity than any ad can fix. Invest in training ladders, cross atelier swaps, and micro automation that removes fatigue but never fingerprints. European production showed resilience as tourist flows returned and spending per tourist held up, yet profitability compressed. The signal is clear that productivity, not price, has to carry more weight.

Governance matters inside craft. Subcontracting chains in Italy have been under intense scrutiny for labor abuses, with authorities placing some suppliers under judicial administration and widening probes. Brands that embed real time supplier audits, wage verification, and tier two visibility will sleep better and spend less on crisis response. The reputational downside is very real and regulators are moving.

After Sales Service & Clienteling

Clienteling is not a contact list. It is a disciplined practice of remembering, predicting, and surprising. Teams armed with unified profiles and tasteful prompts can drive measurable lift. McKinsey finds personalization programs often deliver 10-15% revenue upside, with best in class higher. That applies when messages are timely, consented, and helpful rather than needy.

Digital concierge is catching up to salon level service. Luxury groups are experimenting with generative AI assistants that draft outreach, assemble look suggestions, and pre answer product provenance questions so advisors spend more time on judgment. The point is not bots replacing the client advisor. The point is better preparation and tighter follow through that converts one sale into a relationship.

Innovation That Sticks, not That Drips

Capital is shifting from splashy ecommerce rollouts to gritty improvements across the chain. Fashion and luxury players expect tech investment to roughly double as a percent of revenue by 2030, to around three to three and a half percent. That spend should prioritize three threads. One, supply intelligence that predicts demand by store and client, which means fewer stock outs and fewer awkward transfers. Two, traceability that reduces compliance cost and builds trust. Three, advisor tools that raise close rates without turning stores into call centers.

Clienteling is getting a brain upgrade. Teams now blend qualitative notes with model driven nudges to time outreach around life events or seasonal rituals. Brands testing AI assisted clienteling report faster response times and higher appointment conversion. The risk is tone. Pushy messages read like spam in formalwear. Leaders build style guides into the tools and audit messages weekly for taste.

Traceability is more than a QR code on a dust bag. Evolving European rules on deforestation free supply, circularity, and the coming wave of digital product passports are forcing lot level data all the way back to farms and tanneries. Teams that wire this into upstream systems now will avoid hero projects later. This is not a compliance tax only. It is also a proof point when a client asks where the leather came from and why it costs what it costs.

Assortment strategy is also innovating. Bain notes polarization across brands in 2024, and a flatter personal luxury goods market overall. That calls for ruthless SKU discipline, capsule drops anchored in true craft, and local for local plays as BCG tracks a large shift to local spending in China and a more selective true luxury consumer mindset. Teams that move from calendar driven launches to client driven micro calendars will hold full price sell through longer.

Rules that Bite and Build Trust

Regulatory pressure is not background noise. The EU Corporate Sustainability Due Diligence Directive introduces a duty for large companies to identify and address adverse human rights and environmental impacts across their own operations, subsidiaries, and value chains. That pushes luxury players to formalize risk mapping, grievance channels, and board oversight. Do not park this with legal only. Build cross functional routines so sourcing, design, and retail teams share the same heat map.

The EU Deforestation Regulation covers leather among other commodities and requires geolocation traceability to prove products are deforestation free and legally sourced. That means plot level data, supplier attestation, and documented risk mitigation before items enter the EU market. Luxury brands using exotic leathers or diversified tanneries will feel this most, yet the reputational upside of credible traceability is real when a client asks for provenance.

France banned the destruction of unsold non food products and will fully enforce the rule for textiles and shoes. Inventory strategy must adjust with more cautious buy plans, smarter outlet and resale partnerships, and refurbishment capability in after sales. The days of burning excess to protect price integrity are ending, which is healthier for both planet and P&L.

Italian authorities have ramped up probes into subcontractor practices. Reputational damage spreads faster than any corrective press release, and the financial stakes rise as governments consider certification schemes to safeguard the Made in Italy mark. Boards should ask for tier two and three visibility targets, wage verification rates, and independent audit coverage as often as they review brand heat maps.

Your Board Level FAQ

How do we decide which crafts to scale and which to keep scarce?

Anchor on client perceived differentiation and gross margin by craft. Fund apprenticeships for critical crafts with high contribution and guard those lead times with velvet rope rules.

What is the minimum viable stack for clienteling this year?

Unify identities, preferences, and purchase history. Give advisors assisted writing, next best action prompts, and easy appointment booking. Measure reply time and conversion, not message volume.

Where should we place the first big traceability bet?

Start with materials in scope of EUDR and any high risk labor regions. Require geolocation data from suppliers and test digital product passport pilots on a few hero SKUs.

Do we still need flagships when online grows?

Yes, but roles change. Flagships become theater and service hubs with atelier services, restoration, and community events that feed clienteling pipelines. Treat them like performance media with hard metrics.

How do we reduce returns without neutering client experience?

Improve fit data, visual try on where sensible, and pre purchase consultations for high value items. Incentivize advisors on net kept revenue, not shipped units.

What operating metrics matter most in this slowdown?

Full price sell through, waitlist fill rates, first reply time on client messages, and quality escape rate in repair centers. Mix in store staff retention which quietly drives loyalty and higher tickets.

What is the smartest way to play resale?

Use authenticated brand operated resale to reacquire clients, feed repair teams with parts practice, and manage price ladders. Do not let third parties fully own your legacy products story.

How do we keep design fresh without chasing every micro trend?

Run two clocks. One clock protects brand codes with incremental evolution. The other clock funds small creative labs to explore new materials and collabs, with rapid learn loops into the main line.

Parting Shots from the Atelier Floor

Scarcity without service feels cold. Service without craft feels empty. Leaders that connect workshop, store, and screen with one shared client memory will grow through choppy cycles. McKinsey and Bain both point to a tougher backdrop, which means discipline, not drama, will separate the winners. That tote was not born in a brainstorm. It was born in a system that respected skill and respected time.

Innovation budgets work hardest when aimed at the boring parts of luxury that clients never see. Faster sample to buy loops mean fewer duds. Cleaner supplier data means fewer midnight calls from regulators. Smarter clienteling means your advisors spend less time typing and more time noticing. You feel the flywheel when repairs come back quicker, when VICs hear from you at the right moment, and when stores sell more at full price.

One last nudge. Ask a simple question at your next exec meeting. Where in our chain do we create trust and where do we leak it. If you fix the leaks with the same care you devote to a new leather line, the numbers tend to follow. That is the not so secret truth of luxury.

Artificial Intelligence has moved from experimentation to everyday operations across industries--customer, supply chain, finance, and tech.

Organizations that adopt AI systematically are widening performance gaps in speed, cost, and experience. In McKinsey's 2025 State of AI, 71% of [read more]

Do You Want to Implement Business Best Practices?

You can download in-depth presentations on Value Chain Analysis and 100s of management topics from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives.

For even more best practices available on Flevy, have a look at our top 100 lists:

These best practices are of the same as those leveraged by top-tier management consulting firms, like McKinsey, BCG, Bain, and Accenture. Improve the growth and efficiency of your organization by utilizing these best practice frameworks, templates, and tools. Most were developed by seasoned executives and consultants with over 20+ years of experience.

Readers of This Article Are Interested in These Resources

Most organizations recognize the significant potential in creating value through Digital Transformation. However, they may struggle with the question of exactly how much value they can create and where within the organization the value will come from. This presentation deals with the various [read more]

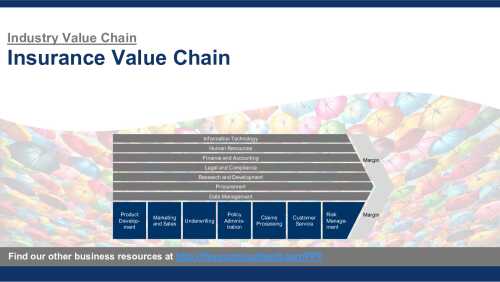

An Industry Value Chain is a visual representation of the series of steps an organization in a specific industry takes to deliver a product or service to the market. It captures the main business functions and processes that are involved in delivering the end product or service, illustrating how [read more]

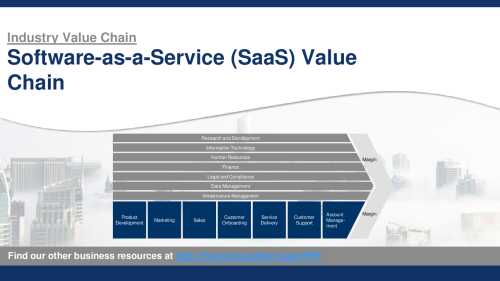

An Industry Value Chain is a visual representation of the series of steps an organization in a specific industry takes to deliver a product or service to the market. It captures the main business functions and processes that are involved in delivering the end product or service, illustrating how [read more]

An Industry Value Chain is a visual representation of the series of steps an organization in a specific industry takes to deliver a product or service to the market. It captures the main business functions and processes that are involved in delivering the end product or service, illustrating how [read more]