Editor's Note: Take a look at our featured best practice, Business Case Development Framework (32-slide PowerPoint presentation). The Business Case is an instrumental tool in both justifying a project (requiring a capital budgeting decision), as well as measuring the project's success. The Business Case model typically takes the form of an Excel spreadsheet and quantifies the financial components of the project, [read more]

* * * *

Editor’s Note: This is an interview originally conducted by Nitiin A. Khandkar of Beyond Quant InvestTraining and published here.

We are pleased to interview John Del Vecchio, CFA, today. Based in Dallas, Texas, USA, John Del Vecchio is the co-founder and co-manager of AdvisorShares Ranger Equity Bear ETF (NYSE: $HDGE) a fund dedicated to shorting individual stocks with fundamental red flags. He is the developer of the Forensic Accounting Stock Tracker. Previously, he managed a hedge fund for Ranger Alternative Management, L.P. utilizing the same strategy. In addition, he worked for well-known short seller David Tice and famed forensic accountant, Dr. Howard Schilit. John graduated summa cum laude from Bryant College with a B.S. in Finance and was awarded Beta Gamma Sigma honors. He earned the right to use the CFA designation in 2001. His website is forensicstocks.com.

John is also the co-author of the book “What’s Behind the Numbers?”, published 2013. So, here’s something common between his book’s title and theme, and the philosophy of my training venture, Beyond Quant InvestTraining – we both seek to go behind or beyond the numbers, albeit in different ways. I’d say that John’s book is a great resource for investors who do not possess forensic accounting skills.

Most value investors use checklists to shortlist stocks for investing. I firmly believe that “Has the company been involved in accounting chicanery?” should be a key item on every value investor’s investing checklist!

The interview is in podcast and transcript formats.

Podcast of Interview with John Del Vecchio

Transcript of Interview with John Del Vecchio

1. Hello John, trust you’re well. Could you tell us about your professional background please?

John: Sure. I started my career in 1997 as an intern for James P. O’Shaughnessy who wrote the book “What Works on Wall Street”. I learned a lot with respect to quantitative methods and testing strategies back to the 1950s.

When I graduated from college I went to work on Wall Street. This was at the height of the Internet boom. I didn’t really like it because it made no sense to me that stocks would go up 1,000% in a day when they had no real business.

I was doing quantitative work in international markets. I didn’t find that particularly challenging. So, I went to go work for The Motley Fool as a writer / analyst. This was wonderful because I was at the cross-section of the Internet and financial markets. The Fool is an online personal finance company. So, I could see first-hand how the markets reacted with Internet companies. While I enjoyed my time there I could see that things would end badly for the Internet boom.

Not too far away was Howard Schilit at CFRA. There I cut my teeth in forensic accounting and learning how to scour financial statements for misdeeds on the part of management. In 2002, I was called upon to move to Texas and start shorting stocks for a new hedge fund. This was soon after September 11, 2001 and the mood of the country back then was to not be afraid to live life. So, I quit my job, sold everything and moved to Texas without ever having been there.

The Internet short trade worked out really well, as well as could be hoped. Soon after David Tice, a well-known short seller offered me a position at his firm. I was there for 5 years before starting a second fund to capitalize on the Financial Bubble. That worked out even better than the collapse of Internet stocks.

We then converted that into an actively management exchange traded fund called the AdvisorShares Ranger Equity Bear ETF (NYSE: HDGE). Later on, I created an index fund which is now the WeatherStorm Forensic Accounting Long-Short (NASDAQ: FLAG). It’s quantitatively based and last year earned a 5-star Morningstar rating.

I co-authored What’s Behind the Numbers? with Tom Jacobs, a friend and colleague from the Fool, and we were honored to be the Stock Trader Almanac best book of 2013.

I had also honed a combination of quantitative factors and forensic accounting and developed my own models. I’ve been approached a couple of times by major Wall Street firms about it, but I am launching the software for all investors. It’s called the Forensic Accounting Stock Tracker™ (FAST) at forensicstocks.com.

2. In the past, you’ve worked with Dr. Howard Schilit, of Schilit Forensics, and short-seller David Tice. What was the most important thing that you learned from each one of them?

John: Howard taught me the importance of analyzing revenue. Conventional wisdom says that revenue is hard(er) to manipulate than earnings. But, that’s simply not true. In my book, I talk about many ways in which management teams can get aggressive with the top line. It’s a very important lesson.

David taught me about strength in your convictions. You can do all the analysis you want, but if you have no conviction, you won’t be successful in your trading by a long shot.

3. Dr. Schilit is the author of “Financial Shenanigans”. The theme of your book “What’s Behind the Numbers?” is similar to that of “Financial Shenanigans”, in terms of its focus on detecting accounting chicanery/fraud. What are the key differences between his book and yours?

John: There’s one major key difference. The stocks discussed in What’s Behind the Numbers? are real case studies done in real-time by me. I was writing research for hedge funds and other institutional investment firms. The reader can see what I saw at the time I was doing the actual work. Then we could look forward and see the outcomes.

I think this is really important. It’s almost like a real-time diary. I have read the other books in the earnings quality space and they were not written in that manner. I wanted to produce something different. I already had a lot of content written, because I had been producing reports for hedge funds for years prior to writing the book.

The market was up every single year while I was with David Tice (where the case studies came from). But, 67% of my targets on the short side were profitable and I was about 1,500 basis points ahead of the inverse of the stock market annually.

In addition, we talk about some methodologies in the book that I have not seen anywhere else.

Alright, great. So, two books – maybe similar theme, but different focus and different strengths.

4. Globally, the biggest and the best businesses are based on the solid foundation of ethics and values. Yet, there seems to be no dearth of companies fudging numbers to achieve a higher market cap. No amount of regulations and penalties seems to curb this. What is your take on this? Is this more of a personal upbringing/psychology issue, than anything else?

John: If someone has a motivation, such as greed, to act aggressively or even worse commit fraud, then no amount of regulations helps to deter that. Forcing someone to certify financial results is really no big deal to the person actively engaging in fraud.

There’s three problems that I see. First, there’s a lot of short-termism on Wall Street.Companies are under enormous pressure to deliver expectations beating results every single quarter. In the normal course of life this is pretty much impossible. Every company experiences a bump in the road. The question is whether management is open and honest about it, or do they try to pull the wool over investors’ eyes.

Second, management’s compensation is often tied to the stock price, but the tenure of an executive is often very short relative to the lifespan of a company. So, if you’re only in a job for five years and you can make $50 million by keeping the stock price afloat before you depart and then the stock crashes, you may be highly incentivized to act in your best interests and not that of shareholders.

Third, generally accepted accounting principles are broad and provide a lot of leeway for management. So, if you have to please Wall Street every quarter, your wealth is tied to the stock price, and accounting is vague enough to use to your advantage, then you can find yourself engaging in questionable activity. Again, that’s the way the market is set up.

Of course, most people aren’t committing fraud. They’re just acting aggressively and using the tools available to them to their advantage. But, over long periods of time that won’t work and shareholders end up getting hurt. So, quality does matter, over time.

5. And usually, like you say it’s the shareholders who’re left in the lurch. In the history of Corporate America, which company would you say was involved in the biggest accounting chicanery?

John: That’s tough to say as there’s been a lot of them. Maybe the most notorious in recent times is Enron. Here’s a company that was huge and powerful. It operated in some of the largest markets in the world. Enron’s leaders were extremely well connected. It wasn’t a mom and pop small cap company selling a single product to a limited market.

In general, I don’t think most people feel that large companies are going to be frauds. They are perceived as being “safe” because they are highly regulated and have top auditors (not an auditor operating out of a suburban strip mall).

I remember reviewing Enron’s financials around the time the stock was about $50 per share. I took the filings home over the weekend to review them. It was insanely complex. The 10-K was hundreds of pages long.

Obviously, it would have made my career at that point had I written a report on Enron. I really had no idea it was a fraud going to $0. I did however know that certain aspects of its business, like revenue, cash flow, and transactions didn’t all add up. But I shied away from it because it was so complex. I tend to gravitate to simple stories that are easy to spot the trouble spots. So, I eventually focused on something else.

In the end it bankrupted the company, put the auditor out of business, thousands of people lost their jobs, retirement savings were wiped out, the city of Houston took a big hit, and people went to jail. I’m not sure of another company in recent history that did so much damage.

Yeah, true. The Enron saga reminds me of my own stint in the US markets way back in 2001. In fact, I did a bit of research on Enron myself in those days – mid-2001 – I think around the time the stock was in the $50-$55 range. I sent across my queries to the IR director at Enron. But their answers were very vague and they tried to present some odd numbers like IBIT per BBTU (billion British thermal units) which were not convincing. Of course, I never predicted that Enron would go down in a bad way in a matter of months. So, Enron was a big shock even to me in those days.

6. You have outlined dozens of ways in which companies try to paint a rosier picture of their finances, in your book. In your experience, which is the single line item in the income statement or the balance sheet or the cash flow statement, which is the most misused, or responsible for the highest chicanery?

John: That’s easy for me to answer – Revenue.

My best ideas on the short side were companies where the revenue presented was not sustainable. The classic example is offering better terms to customers to sign a contract today that otherwise would have been signed at a later date. The result is pulling forward revenue that would have been booked in a future quarter into the current period.

This is effectively stealing from the future. Now that the revenue has been pulled forward a new customer must be found to replace that future revenue. But, if demand was strong for a company’s products in the first place, then there’s no incentive on the part of management to act aggressively on the top-line. So, it just takes care of itself.

And, revenue is the top-line. Everything flows from the top down. Plus, it often directly relates to the demand for a company’s products and services. There’s no better indicator of trouble than when management is overstating its sustainable revenue growth. That’s the most aggressive action they can take, in my opinion.

7. In your book, you’ve discussed the “stuffing the channel” tactic, and how you called out eResearch Technology for increased days of sales outstanding (DSO), around March, 2006, when the price was ~$14. The stock crashed all the way down to $6 later that year, and the company was ultimately taken private in 2012 at a price of just $8 per share. I guess you want to quickly discuss that case?

John: Sure. This was a pretty simple story. Simple stories tend to work very well. There was not much justification needed to want to short the stock. It had all of the elements of something not right.

First, they stuffed the channel.What that means is that they acted aggressively to recognize revenue.By pulling that revenue forward it increases the risks in future quarters that they will have a revenue shortfall.

In addition, there were a couple of key management departures. People leave companies all the time for a variety of reasons. But, I felt like the timing of the departures was of interest because they had acted aggressively on the top-line, in my opinion. So, I was concerned about the demand for their product.

Finally, the expectations had been pushed entirely onto the second half of the year. They were going to have to have their best 6 months ever in order to make those numbers. Based on my analysis of revenue quality, there was no way that was going to happen. Management knew it too. Hence, they bailed out of the company. And not long after that, the stock imploded not long after and was a big winner for us.

I agree, John. You mentioned the departure of key management personnel. Coming back to Enron, I recall that the CEO, Jeff Skilling had left the company sometime in August, 2001, just 3 months before the company filed for bankruptcy. So, that’s a huge red flag, I’d say.

John: Absolutely!

8. In general, which has been the starkest example of accounting chicanery that you flagged or called out in your career, as covered in your book?

John: AsiaInfo-Linkage ($ASIA) was a great story. Ultimately the stock plunged 60-70%. Although it wasn’t without some pain first on the short side. It ran up pretty good on me, when I first starting questioning their financials. Simply, the numbers didn’t add up.

They were using percentage-of-completion accounting which can allow for aggressive revenue recognition and potentially overstate profit margins. Basically, you book the revenue in advance of billing the customer. The issue is not whether the company will collect on the receivable, but rather the timing of revenue recognition.

Management could get aggressive and estimate that much more of the contract is completed than is really the case and front load that revenue. They could also overestimate the profitability of the work to that point. So, you get revenue growth and margin expansion.

Once I saw that the math didn’t add up, I knew immediately that this would be a great short. It really only took me about five minutes of work to figure that out. Of course, I spent a lot of time understanding it better, but I knew right away that this was a ripe idea.

Revenue was overstated, margins were overstated, and earnings quality was very poor. There’s a case study in my book about $ASIA.

9. Could you briefly discuss the cash-flow and inventory jugglery?

John: Inventory gets companies in trouble when it ages and the product needs to be sold. So, profit margins will often take a hit as a result. As the inventory is building, the company may get a boost to profit margins as they spread out costs relative to production. Or, they may sell written off inventory at a later date. That creates an artificial margin boost.

Tracking working capital (inventory, receivables, and payables) every quarter for companies you are interested in is a good way to spot when they may be starting to have some trouble. Years ago, Deckers ($DECK) was a short position because the inventory build-up was much higher than management indicated and their cost inputs were rising dramatically, but they could not pass those along to the customer – they couldn’t raise prices. In addition, they did some things that were aggressive on the revenue line. So, you kind of see a common theme there – change of revenue recognition policy.

So, it was a classic case of slowing demand which led to the income statement getting compressed. It was a core growth stock for many growth managers in the US, that eventually got hammered.

As far as cash flow goes, work needs to be done to make sure the cash flow being reported paints an accurate picture. For example, if a company makes a big acquisition, operating cash flow benefits from the liquidation of inventory and collection of receivables, but the cost is an investing cash flow. So, cash flow needs to be adjusted to reflect that.

Another example is if there’s a one-time item in the cash flow statement. It might provide an unsustainable boost.

So, don’t just take cash flow as fact. It requires work to make the adjustments.

10. Can you discuss in detail a few recent examples of companies engaging in accounting chicanery, which you came across (or uncovered) after your book was published, which were of substantial magnitude? What was your estimate of the earnings impact, of such accounting jugglery?

John: I’m not a fan of $IBM. I think IBM is the classic example of a company that massages the numbers from quarter to quarter. Imagine if you told someone a few years ago, that IBM would have five years of declining revenue, they would think you were crazy.

But, that’s what happened. In the meantime, their receivables trends were moving the wrong way. In some cases, they missed revenue estimates by $500 million – $1 billion, despite potential channel stuffing. One rarely knows for sure what motivation they have, so we can only use the financials as a guide to make an educated guess. Then they used tens of billions of dollars to buy back stock and protect the dividend, while cash flow performance was poor. They also are very crafty at using the tax rate to their advantage to find earnings per share. Buying back stock, manipulating the tax rate.

The term for this is Financial Engineering. And, it hasn’t worked. IBM’s stock is nowhere near its high, while the broader markets are at highs or very close to them. I think the gig is up for IBM.

When you use tens of billions of dollars to buy back what turned out to be overvalued stock, that’s very defensive in nature. They didn’t allocate capital to grow their business. That money is now spent.

So, they are chronic users of accounting to their advantage. I think everyone knows it now though.

I’d like to point out another example. It’s not so much an accounting jugglery situation though. Rather, it’s a case where a great company can be a bad stock. That stock is Under Armour ($UA).

For quite a while, before the stock blew up, it was ranked as the lowest stock in my Forensic Accounting Stock Tracker. So, somebody needs to be the worst to happen to be there!

It’s not that management did anything illegal. Rather, the warning signs were flashing deep red. The working capital was moving in the wrong direction. Inventory was building. Receivables were lengthening and cash flow was deteriorating.

Under Armour was a key holding for growth stock managers. But, when things start to go wrong, the downside to these types of stocks is significant. Those managers aggressively start selling the stock. I like Under Armour’s products, but the facts are that the working capital build up was signaling a slow-down in demand and margin compression going forward.

Sometimes business hits a wall and adjustments need to be made. There can be bad businesses that can be great investments. It depends on expectations, quality of financial presentation, etc. Sometimes ugly stocks make beautiful investments. In this case, it was an overly owned growth company, where the warning signs were flashing red.

11. How has the Del Vecchio Earnings Quality Index performed v. the S&P 500, after 2011?

John: It’s done well which is interesting because I think the market has rewarded excessive risk taking in recent years. However, the stocks that score at the top have continued to do well like 2014 and 2016 in particular, were bumper crop years.

The results of the stocks on the bottom end of the spectrum have been mixed. There’s been some that have done well, again because market’s rewarding speculative purchases, but also a lot of stocks that have performed poorly. So, there were rewards for not being invested in them.

I use software which I call the Forensic Accounting Stock Tracker to analyze baskets of stocks, sectors, and individual companies. It’s been refined recently, but the general concept remains the same. That is that the less incentive there is on the part of management to manage earnings from quarter to quarter, the better the stock typically performs.

12. John, could you give an overview of the long-short strategies your book mentions?

John: In the book, we looked at my record running a hedge fund as a short seller and Tom’s recommendations on the long side. We don’t manage money together. Tom is a value investor and we were showing what might be possible by using both sides of the market, because people tend to be very focused just on buying stocks.

Since then, a firm called Vident created the WeatherStorm Forensic Accounting Long-Short index. There’s an ETF that uses the index under the ticker symbol FLAG, for red flags. The fund is 130% long and 30% short.

Vident verified my own work and manages the fund. An interesting aspect of Vident is that they believe in values based inventing. So, factors like good corporate governance and ethics play a role in the companies that they analyze and invest in. Along those same lines is clean accounting, which is what I am focused on, and which is why they liked my work so much.

13. That’s interesting. What attributes make a stock a candidate for shorting, in your view, apart from the valuation itself? Do you short purely on the valuation?

John: I’ve never shorted on valuation. Some of the best shorts are value traps. I think the best candidates have aggressive revenue recognition. Other warning signs are working capital issues like inventory buildup.

The more factors affecting the demand for a company’s products, the better. If a company reports earnings and they beat estimates by a penny because they bought back some stock, no one may care. If they miss revenue estimates by $100 million because demand is starting to fade, the stock could get crushed.

So, it’s trying to figure out what’s driving that financial performance and whether anyone will care if the company falls short of those expectations.

14. Coming to your hedge fund, viz., AdvisorShares Ranger Equity Bear ETF ($HDGE). Your fund’s mandate is to short individual stocks. Could you discuss your shorting strategy – how you go about identifying companies with red flags, how do you actually do the shorting, for how long you would usually keep the short position open, etc.?

John: Right. So, we focus on U.S. stocks and ADRs. We’re looking for aggressive accounting or fundamental deterioration in a business. Typically, we hold about 40-50 positions. We do not use any leverage. We are not an inverse fund so we are not designed to track the inverse of the S&P 500, for example. We’re just a collection of short positions.

The benefit of that is we pick individual stocks. The S&P is market cap weighted, so when you short the S&P, you’re shorting companies like Apple or Johnson & Johnson. And you have to ask yourself, do you want to be short them? Maybe. But, maybe you don’t.

Instead we are focused on companies we think have problems.

Historically, that has led to more downside capture when the market pulls back. For example, when the S&P 500 had a 7% draw down, our fund was up a little over 15%. Again, we don’t use any leverage.

We come about ideas in many ways. I’ve had the benefit of working with some great people that are talented at reading financial statements. We use 3rd party research and then confirm it with our own analysis.

All the work that we look at is based on information that is available to the public. It’s all there in the filings. Some of the best ideas then are hidden in plain sight.

I’d say red flags come in many forms. As I mentioned before, revenue recognition, working capital, and quality of cash flow are some of my favorites. They tend to be simple stories. Simpler is often better.

In all cases though, we borrow the stock from our prime brokers and then sell the stock. Our positions tend to be 1-4% in size. My co-manager, Brad Lamensdorf is focused on technical analysis.

So, if a stock is rallying, we might scale back the size and wait for a better spot to be more aggressive. If the overall market is rising sharply, there might not be much we can do. As you said, our mandate is to be short, so it’s kind of it is what it is.

The same can be said for when stocks are falling. We will pay attention to which stocks are staying stronger and trim them. If the selling is broad based, then we may do nothing and just sit on our hands. So, from that perspective, we’re tactical in nature.

15. $HDGE has underperformed its category over the last 1 year or so. Is this underperformance attributable primarily to the rally in the US markets? Have you recently uncovered any red flags in companies in which you have short positions?

John: We are the only pure short actively managed ETF. So, I’m not sure there’s really a category that’s valid. The average stock was up about 20% in 2016 and the highest shorted stocks were up over 30%. So, we held in there just fine. We were much closer to having a great year, but suffered a couple of acquisitions that hurt us.

I’m not really worried about 1 year performance or even past performance. I think one needs to focus on the future. The longer the current bull market rages (it’s one of the longest in history, I think the second longest bull markets in history), the nastier the next bear market will be. That’s always been the case.

This market has been propped up by very low interest rates and financial engineering. It can go on a long time, but it never ends well.

That makes it tough to short stocks but we are a short selling fund so that’s what we do. In the mid- 2000s, even though the market was going up every year there were wonderful opportunities to short stocks. And, interest rates were higher which helped returns because the cash from the short sales could earn interest. That really hasn’t been the way since 2010, when the Federal Reserve explicitly targeted higher stock prices. But, those times will come around again someday. And it will be more attractive to short stocks in bull markets.

There’s always companies that have red flags. The beauty of an ETF is that all the positions are publicly disclosed. So, anyone can see them. So, you can go on the internet and get our positions.

I’d say one theme we have now is credit as it relates to autos and auto finance. There’s a bubble forming there in my opinion.

The other bubble in my opinion is the passive indexing bubble. The move into index funds and away from active management is creating massive overvaluation. The median price / sales ratio on the S&P 500 is the highest I have ever seen. Profit margins have peaked and a lot of other factors can lead to substantial downside.

In 2002, technology stocks were dominating the market and skewed the valuations to extremes. Underneath that there was a stealth bear market in non-tech stocks. So, when the S&P 500 cracked in 2002, there were actually a lot of stocks that performed well. The index was too top heavy in technology.

In 2007, it was financials. More stocks got carried out with the bathwater in 2008, but they also bottomed ahead of the broader indexes in early 2009, which set up some great opportunities.

My fear now is that there is nowhere to hide. Everything has been propped up. So, the next one will be particularly nasty.

16. I guess the ride has to slow down somewhere and as they always say, “some guys will be left with no chairs when the music stops”. $HDGE currently trades at a 52-week low. What is your take on U.S. stocks in general? After this rally spanning the last few months, do you expect a correction? Which would be your favorite stocks to short, at this point in time?

John: Since the election here last November, it’s been almost impossible to be short stocks. Expectations are very high for the new president. But, even the setbacks he has had haven’t seemed to matter. Stocks roar higher. The more speculative the stock, the higher it goes.

In general, though, valuations are among the richest in modern history. Profit margins have peaked. Stock buy backs were a huge factor in pushing stocks higher. But, corporations have started to pull back. Retail investors bought ETFs at a record pace in recent months. But, that is starting to slow a bit as they probably run out of fresh capital. Margin debt is significantly higher than it was in the last two crises. Market sentiment is too high. So, high sentiment and negative credit balance is usually a recipe for disaster. Meanwhile, insiders are selling at the fastest pace in years. NYSE margin debt has exploded. Investors’ negative credit balances are substantially higher than the last two market peaks.

But, the market seems to go up just about every day. However, I think the easy money has been made and whatever gains we have from here will be lost and then some. What we are missing is a catalyst to cause everyone to flee stocks at the same time. That adds to the challenges.

Our portfolio is available to the public. I want to refrain from picking on any particular company at this point, don’t want to bash up anyone. I will say we are very aggressively positioned on the short side, though with near maximum exposure and beta in the portfolio. So, we’ve got a lot of rocket fuel in the portfolio right now.

17. Have you looked at Amazon ($AMZN)? While the stock appears expensive on the basis of historical earnings, markets seem to have factored in the potential of its new businesses like AWS. What are your views and would you consider shorting $AMZN, given the valuation of upwards of 70x-75x forward earnings?

John: No, I’m not interested in shorting Amazon at this time. In fact, I’m more interested in shorting the anti-Amazon’s at this point. One of the themes of our portfolio is shorting traditional retail as well as the mall operators. We’ve a big exposure to mall operators.

There’s a lot of companies that would have to massively close the number of stores to get their sales per square foot back to where it was 10 years ago. It’s a trend that is picking up steam. And, in my opinion we are very late in the current cycle so that could make things worse when the broader economy weakens (it’s already been one of the worst economic recoveries ever). The GDP number last week was not very good, so that’s something to pay attention to.

Ralph Lauren just closed a big store in New York City. They pay almost $70,000 a day in rent and signed a $400 million lease. So, they would rather pay $70,000 a day in order to not have employees and other costs and not generate any revenue. It’s prime real estate in New York too. It’s truly amazing when you think about it.

So, I don’t see the point in trying to pick the top in Amazon when there’s a lot more obvious places to look for companies having problems due to Amazon’s success!

Yeah, in fact I read about the auto dealers not being interested in keeping cars in the showrooms, because of the real estate angle these days.

John: It’s tough to do business in the brick-n-mortar fashion, no question about it.

18. One last question, John, on the accounting chicanery side. As I am myself from an accounting background, just need your views. What are your views on the overall quality of the accounting or auditing firms? You know, the SEC requires the accounts to be audited and blah blah blah. What exactly is going wrong? How come the companies are able to get away with accounting chicanery?

John: So, I think there’s a lot of grey areas in accounting. It’s so wide you could drive a bus through it. Obviously, in the early 2000s, when there’s a lot of these like Enron and Tyco – the accounting firms were getting paid huge amounts of money to do consulting as well. So, there was a sort of inherent conflict of interest there, and even today, when it comes down to certifying financial results and what not. But as I mentioned earlier, if someone’s motivated to commit fraud in extreme case, then asking them to sign a paper isn’t going to do much.

I just think there’s so much vagueness to what’s going on that the auditor’s not going to necessarily dig AsiaInfo Linkage for using percentage completion accounting and booking more revenue upfront. The management team may be able to justify that. And again, it doesn’t have to do with the collection of revenue, but as to the timing of it. And so, because there’s a lot of ability to estimate on the part of management, it’s really hard to kind of pinpoint where they’re going wrong, or committing a sin of some sort. Accounting is just not black and white. If it was, maybe it would be a lot harder for people to engage in this activity, but it’s not, so they do!

Okay, John, it’s been very enlightening and interesting to hear your views about topics related to accounting chicanery and no doubt your book makes great reading, and I’m quite sure my readers will get a lot of value from this interview. So, thanks again, and it was nice to have you here today.

John: Great, thank you so much, it was great to be here. Bye!

This is a financial model used to prepare and analyze the financials of any business venture.

The model includes:

- 10 year financial/cash flow forecast

- Standard NPV, IRR, Payback metrics etc.

- Economic value added analysis

- Analysis charts

- Side-by-side scenario analysis (up to [read more]

Do You Want to Implement Business Best Practices?

You can download in-depth presentations on Financial Modeling and 100s of management topics from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives.

For even more best practices available on Flevy, have a look at our top 100 lists:

These best practices are of the same as those leveraged by top-tier management consulting firms, like McKinsey, BCG, Bain, and Accenture. Improve the growth and efficiency of your organization by utilizing these best practice frameworks, templates, and tools. Most were developed by seasoned executives and consultants with over 20+ years of experience.

Readers of This Article Are Interested in These Resources

This is an excellent training material on developing financial models. This presentation includes the following content

1. Introduction

2. Model development process

3. Planning

4. Business logic design

5. Spreadsheet design

6. Data gathering

7. Testing and developing insight

8. [read more]

The Complete Guide to Financial Modeling: Mastering the Art of Data-driven Decision Making

Introduction:

In the dynamic world of finance, accurate and effective financial modeling is a crucial skill for professionals seeking to make informed business decisions. This comprehensive guide, [read more]

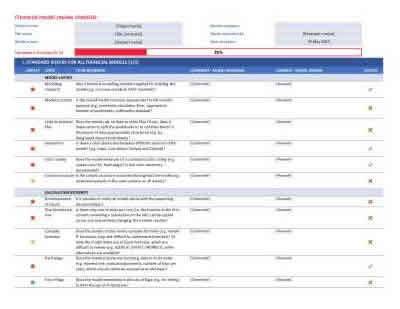

Large-scale financial models are time-consuming. Financial models are an integral part of the business decision-making process, enabling organizations to assess the financial implications of commercial decisions with confidence.

The construction of a robust financial model is the cornerstone of [read more]

Our checklist is intended for all kinds of financial models: M&A models, valuation tools, liquidity forecasts. You name it. It covers standard checks, which are applicable for all financial models like the following:

- Which financial modelling standard was applied?

- Is the model's structure [read more]

We are pleased to interview

We are pleased to interview