IFRS 9 Expected Credit Loss Premium Model – Excel XLSX

Excel (XLSX)

BENEFITS OF THIS DOWNLOADABLE EXCEL DOCUMENT

- Provides a structured IFRS 9 ECL framework using PD, LGD, EAD, staging, macro scenarios, and probability-weighted credit loss calculations.

- Helps finance, credit risk, audit, and reporting teams analyze impairment allowances with dashboards, stress testing, and validation checks.

- Saves time by providing a fully editable Excel model that can be customized for different loan portfolios, assumptions, and reporting periods.

FINANCIAL RISK EXCEL DESCRIPTION

This IFRS 9 Expected Credit Loss Premium Model is a comprehensive, ready-to-use Excel-based framework designed to help financial institutions, lenders, credit teams, finance departments, auditors, consultants, and risk professionals calculate, analyze, validate, and present Expected Credit Losses under the IFRS 9 impairment approach.

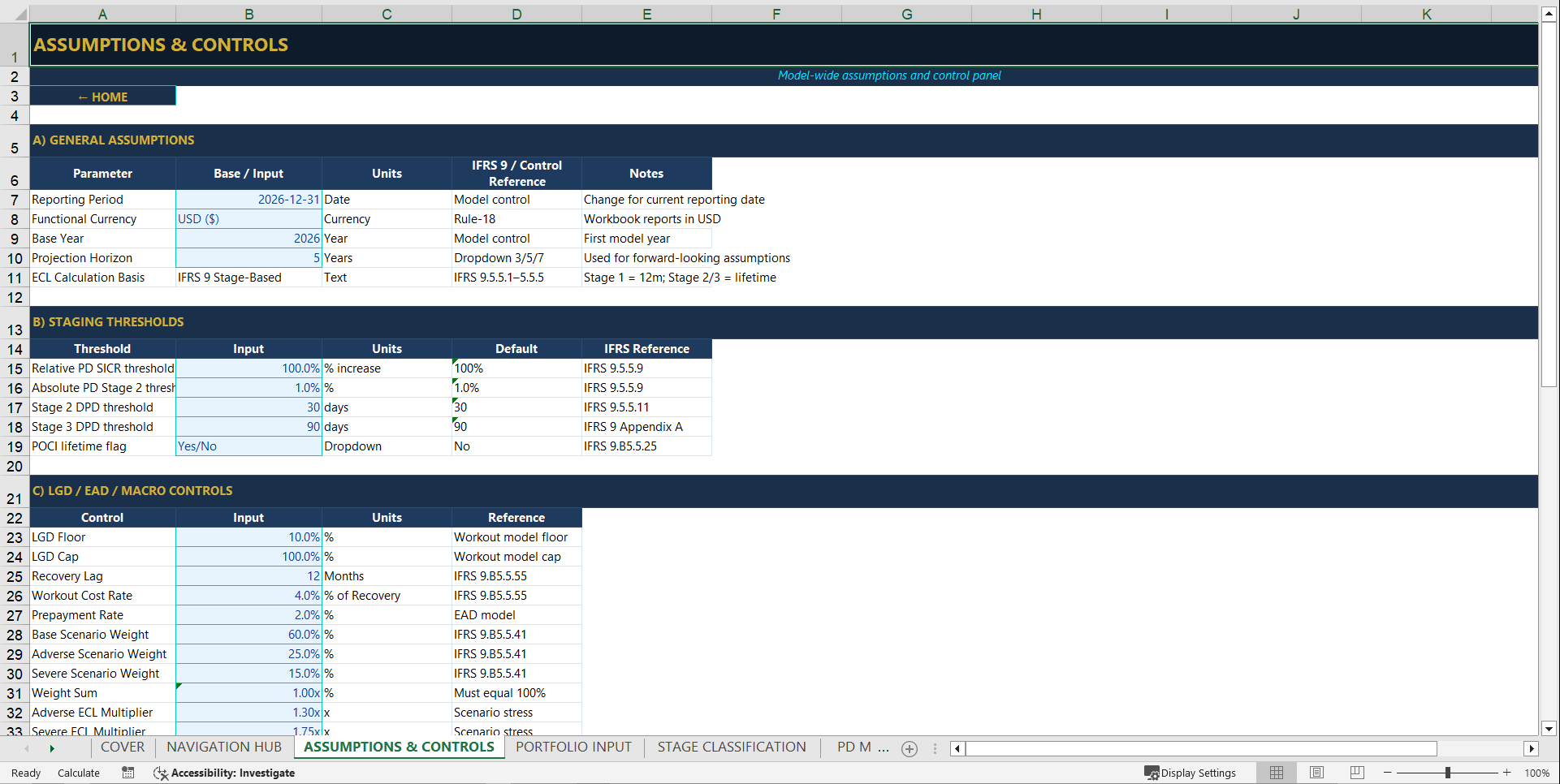

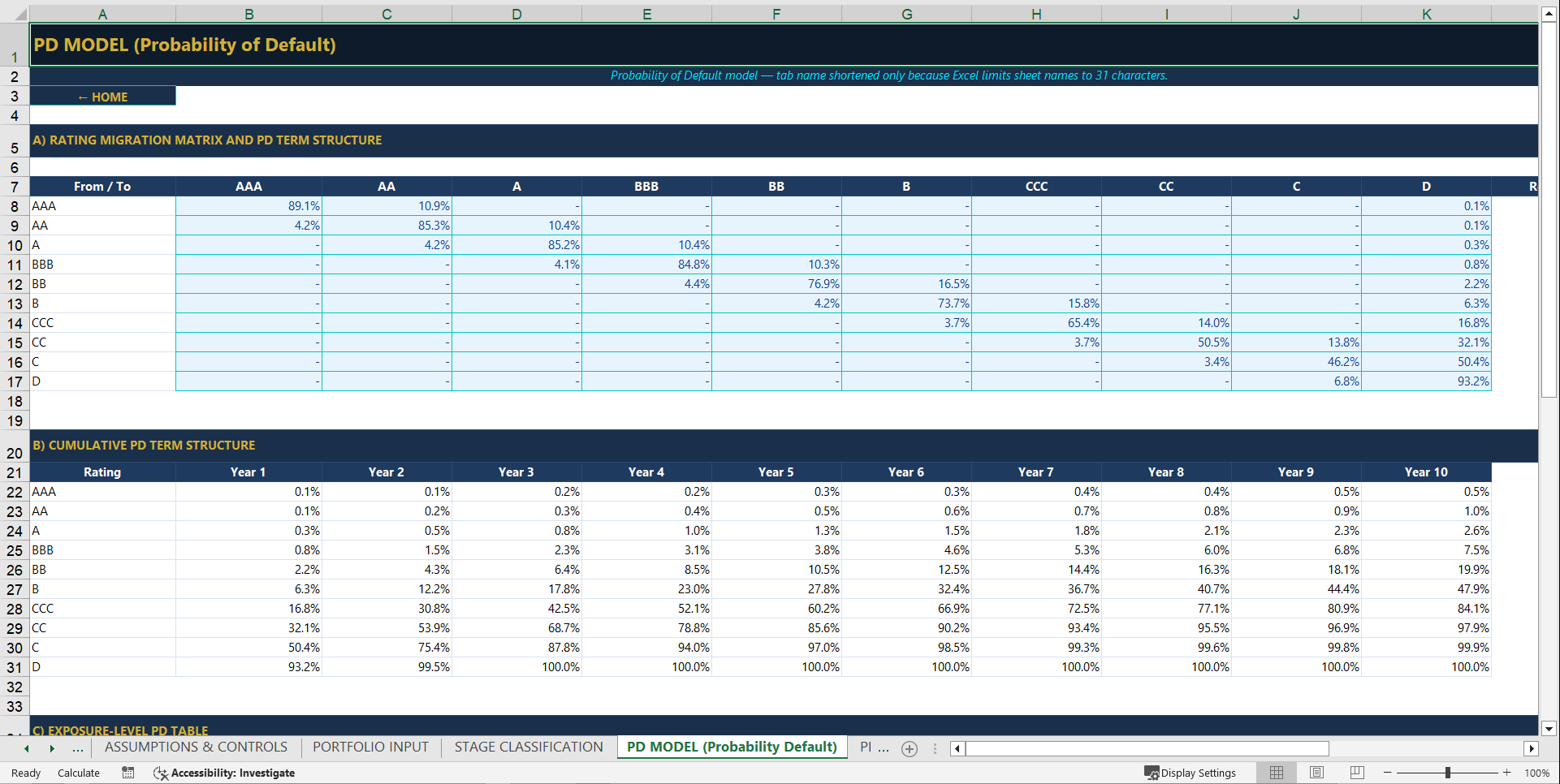

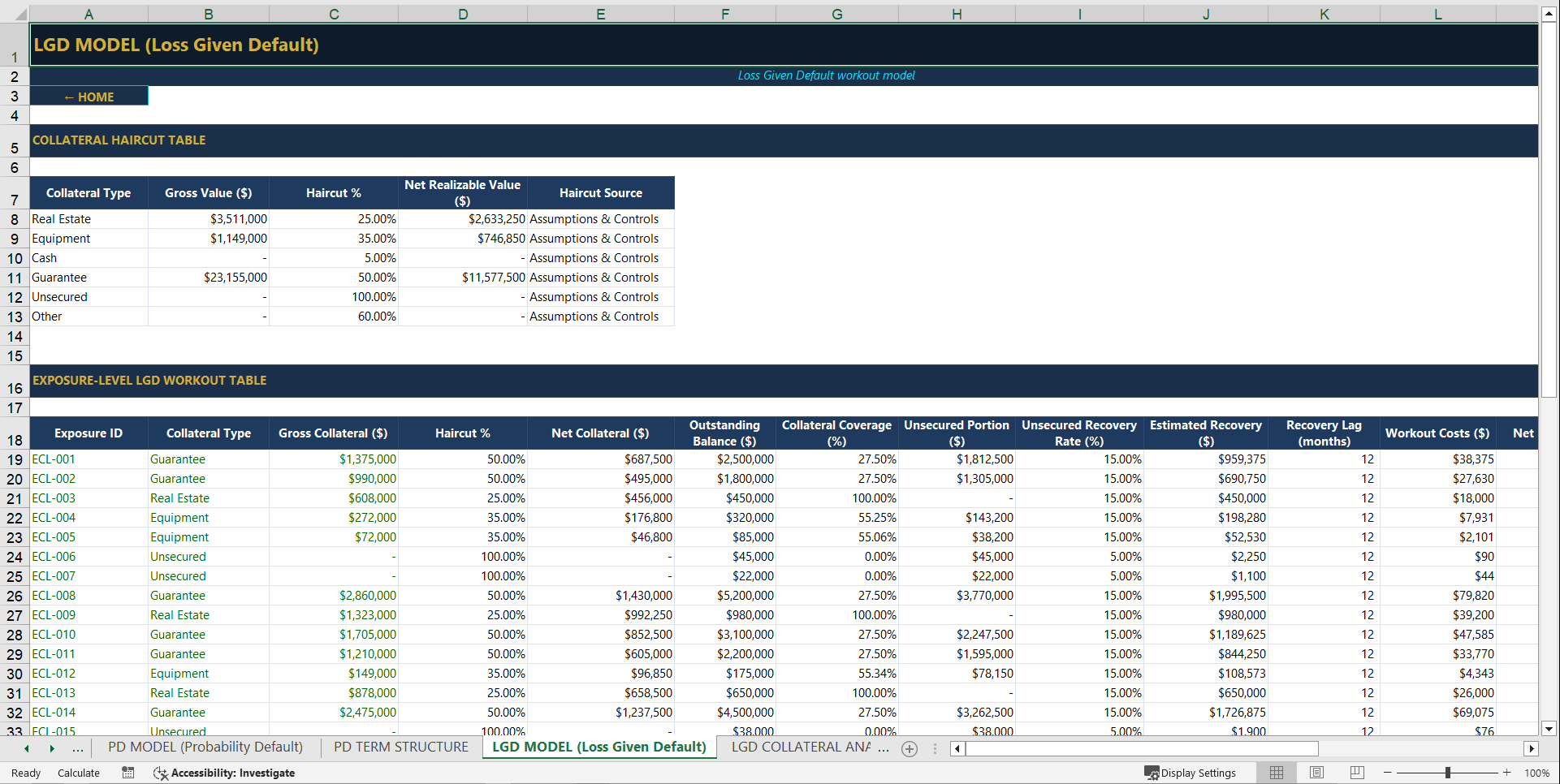

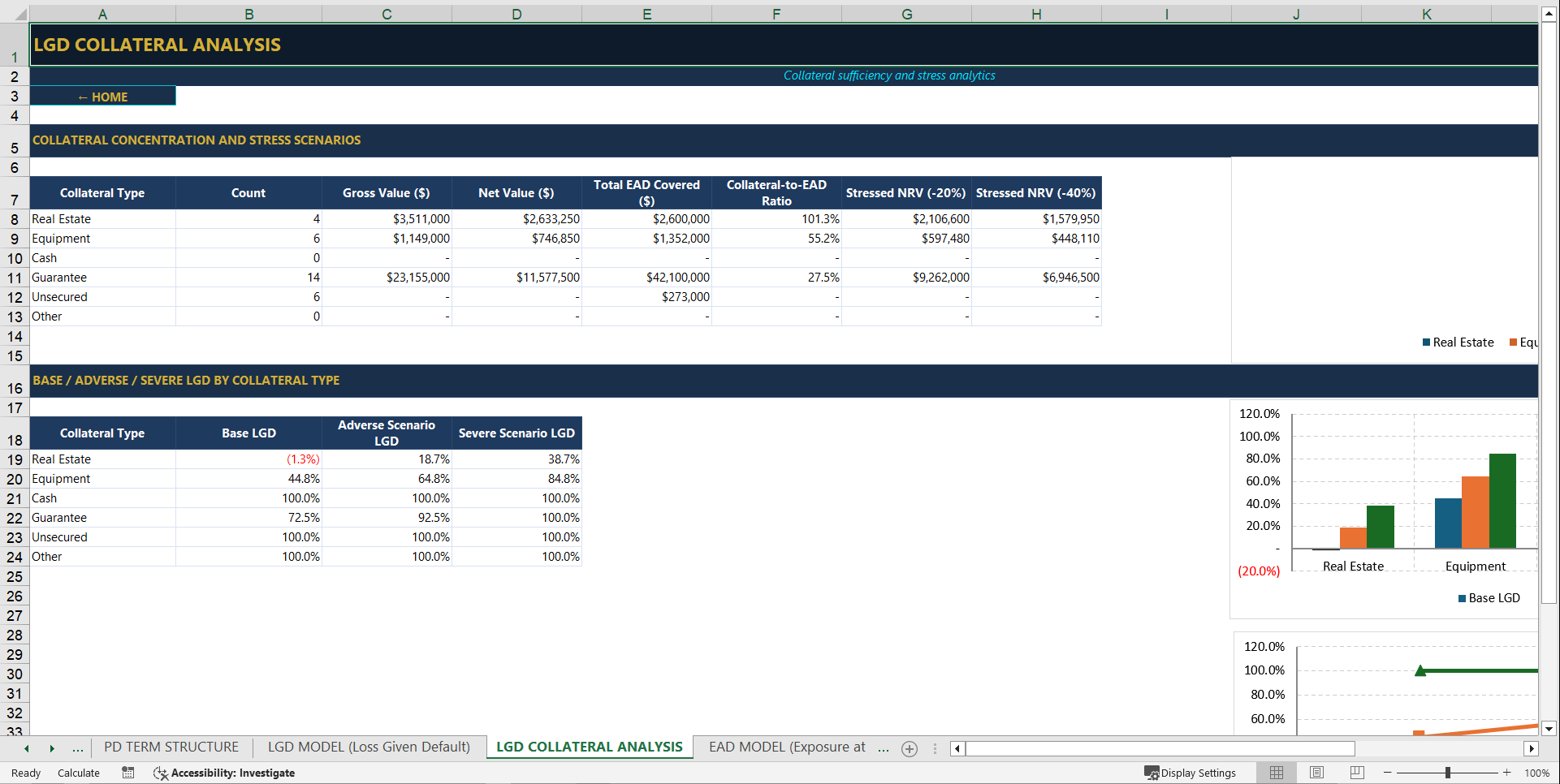

The model is built around the core IFRS 9 ECL methodology: Probability of Default (PD) × Loss Given Default (LGD) × Exposure at Default (EAD), adjusted for staging, macroeconomic scenarios, forward-looking information, collateral recovery assumptions, and probability-weighted outcomes. It provides a structured workflow from portfolio input to final ECL calculation, allowing users to assess credit risk exposure at both individual borrower and portfolio level.

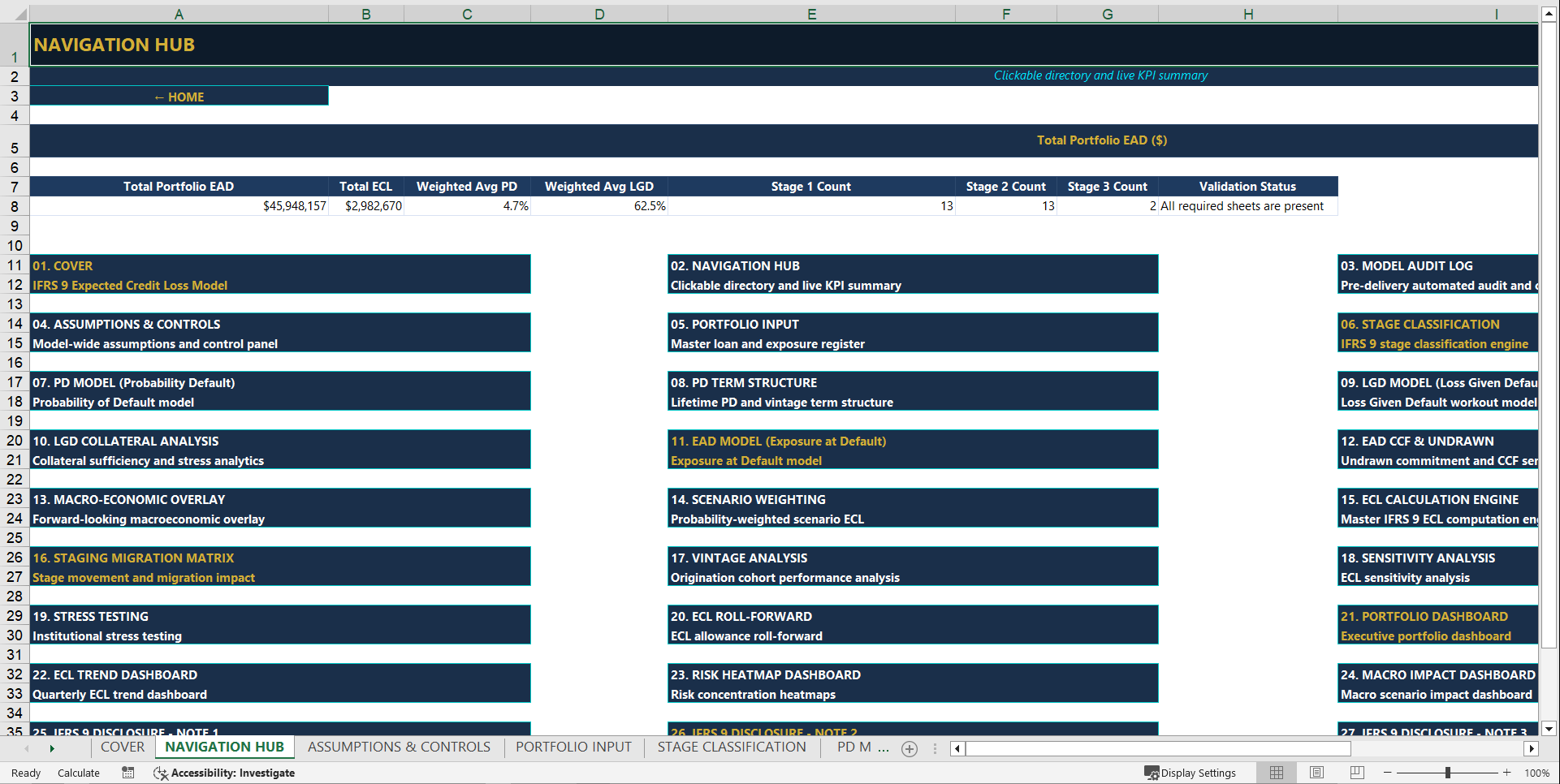

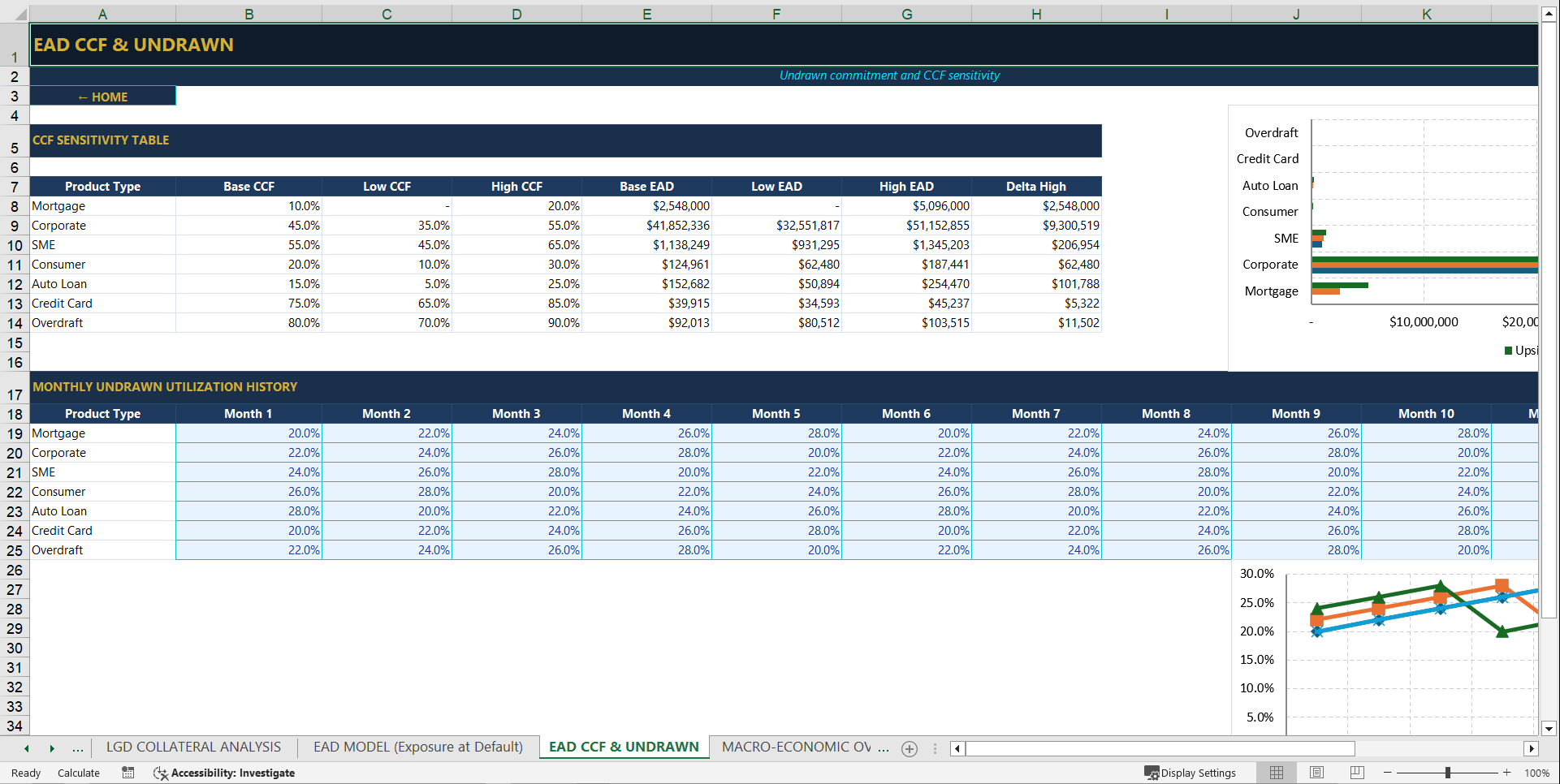

The workbook includes dedicated modules for portfolio input, stage classification, PD modeling, PD term structure, LGD modeling, collateral analysis, EAD calculation, CCF for undrawn commitments, macroeconomic overlay, scenario weighting, ECL calculation engine, staging migration, vintage analysis, sensitivity analysis, stress testing, ECL roll-forward, dashboards, disclosures, audit trail, validation checks, glossary, and version control.

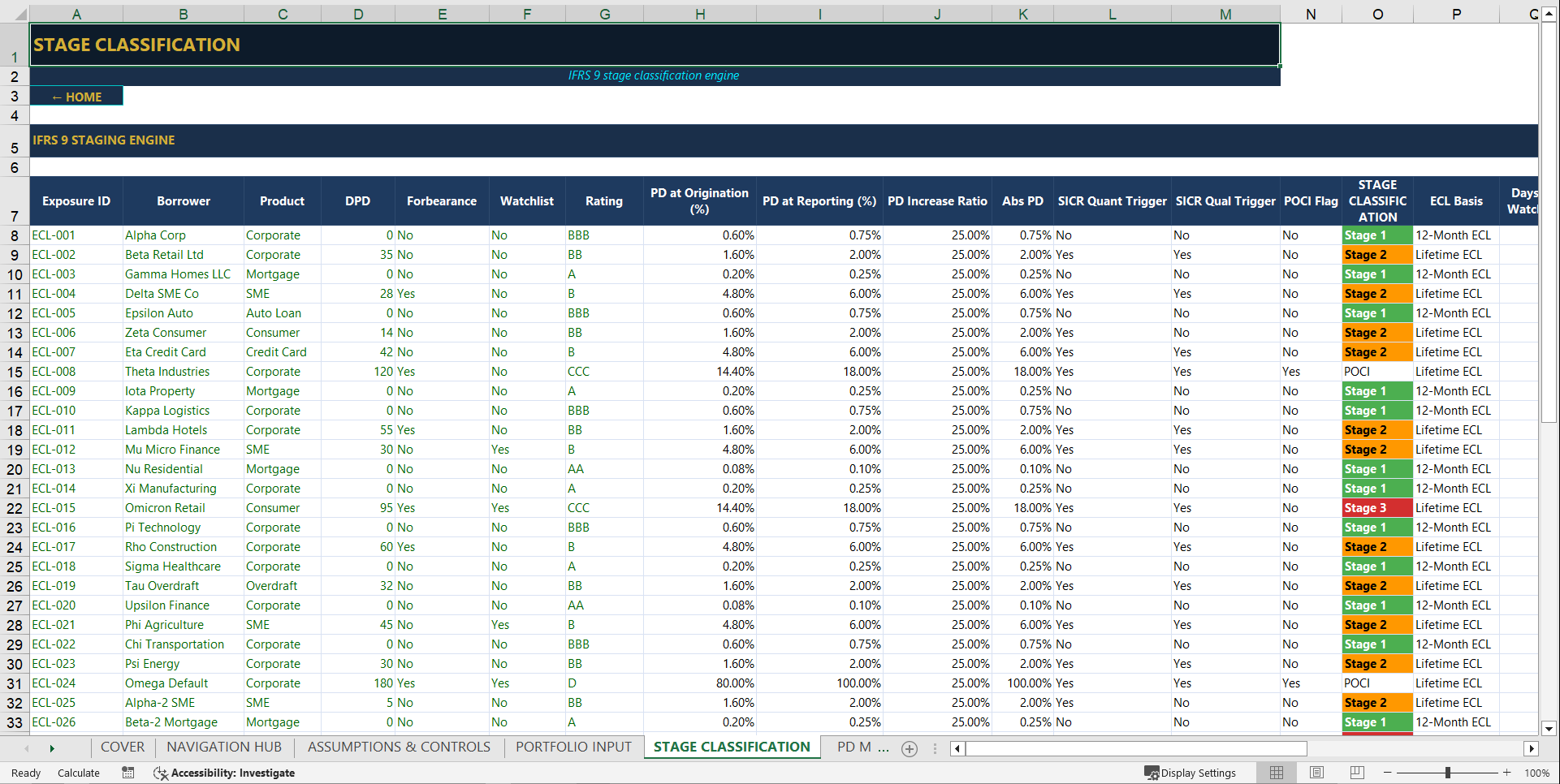

Users can enter or update loan-level data such as borrower name, product type, rating, industry, country, outstanding balance, undrawn commitment, collateral type, collateral value, days past due, forbearance status, watchlist flag, interest rate, remaining maturity, amortization type, write-off flag, and POCI flag. The model then classifies exposures into IFRS 9 stages and calculates 12-month or lifetime ECL depending on the credit risk status of each exposure.

The model also includes forward-looking macroeconomic scenarios such as Base, Adverse, and Severe cases, with probability weights that feed into the final probability-weighted ECL. This makes the model useful for management reporting, impairment analysis, credit risk reviews, audit support, financial reporting, and scenario-based risk planning.

Built-in dashboards summarize key outputs including total EAD, probability-weighted ECL, coverage ratio, weighted average PD, weighted average LGD, top exposures by ECL, macro impact, risk heatmap, and ECL trend analysis. The included sensitivity and stress testing sections help users understand how changes in PD, LGD, EAD, macro assumptions, scenario weights, and CCF assumptions affect expected credit losses.

This model is best used by banks, NBFCs, lending institutions, credit portfolio managers, risk consultants, auditors, finance teams, and IFRS reporting professionals who need a practical and structured IFRS 9 ECL calculation template. It is fully editable and can be customized for different loan portfolios, product types, reporting dates, currencies, risk ratings, and internal credit policies.

The workbook also includes IFRS 9 disclosure note templates, methodology references, audit trail checks, validation status, and a glossary of key terms, making it suitable not only for calculations but also for documentation, review, and presentation purposes.

Got a question about the product? Email us at support@flevy.com or ask the author directly by using the "Ask the Author a Question" form. If you cannot view the preview above this document description, go here to view the large preview instead.

Source: Best Practices in Financial Risk, Integrated Financial Model Excel: IFRS 9 Expected Credit Loss Premium Model Excel (XLSX) Spreadsheet, PDMM Financial Models

ABOUT THE AUTHOR

PDMM Financial Models helps business owners, entrepreneurs, investors, consultants, analysts, and finance professionals make better decisions through practical, structured, and professional financial models.

We specialize in creating Excel-based financial models for business planning, valuation, forecasting, feasibility analysis, investment analysis, project finance, budgeting, fundraising,

... [read more]

Ask the Author a Question

You must be logged in to contact the author.